While we are on the topic of cutting government budgets, Angela Merkel has also announced some draconian measures in Germany. Observers are now asking about the Canadian fiscal “miracle” (see discussions here and here). To me, it doesn’t feel like a “miracle”, but happenstance that was the result the combination of austerity, a bull market and the decision not to go overboard on military expenditures. Recall that at the end of the Clinton era, both the American and Canadian fiscal budgets were in surplus, artificially buoyed by capital gains from the Tech Bubble market. In the wake of 9/11, the US embarked on a series of military adventures and keeled over into deficit, while Canada only made a limited commitment and remained in surplus for a few more years.

Putting any cuts into perspective

It is beyond the scope of this post to comment on the pros and cons of fiscal tightening at this stage of the economic cycle. That dilemma is not insignificant but further discussion of those issues will have to be delayed to another day. Nevertheless, to the deficit hawks who are reading this, I would caution that you should put any budget cuts from any government into the following perspective.

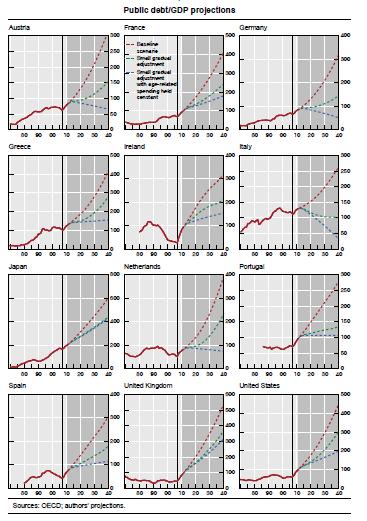

I had discussed the BIS report entitled The future of debt prospects and implications before. The chart below is from the report and shows the projected debt to GDP ratios of Europe, Japan and the United States for the next 30 years. The red dotted line depicts the baseline scenario, which assumes that assume that government total revenue and non-age-related primary spending remain a constant percentage of GDP at the 2011 OECD projected levels. The green line assumes budget cuts of 1% of GDP for five years starting in 2012. The blue line assumes deeper cuts to entitlement programs, e.g. pension benefits, etc.

The UK chart on the bottom row shows budget balances spiraling out of control in all three scenarios. By contrast, the announced German cuts amount to about 0.7% of GDP per year for the next four years, which falls short of the BIS projection of 1% of GDP.

A framework for analysis

Budget cutting isn’t easy for fiscal authorities. Paul Krugman characterized the US government as a giant insurance company with a military. The key items to watch are the cuts to entitlement programs (i.e. pensions, health care benefits, especially given the higher demands of an aging population). Paul Volcker recently raised the issue of dealing with these long-tailed liabilities of government because "the time we have is growing short":

Restoring our fiscal position, dealing with Social Security and health care obligations in a responsible way, sorting out a reasonable approach toward limiting carbon omissions, and producing domestic energy without unacceptable environmental risks all take time. We’d better get started. That will require a greater sense of common purpose and political consensus than has been evident in Washington or the country at large.For investors, evaluating the effectiveness of any fiscal austerity program isn't easy either. It can be hard to cut through the ideological noise and baggage that burden all of us. However, things become much clearer once we use the analytical framework as outlined by the BIS report.

No comments:

Post a Comment