It it with some alarm that I am seeing more instances of investment pundits expressing their political views. In such cases, I start to wonder whether their politics are affecting how they invest. It can lead to an attitude of "the policy is wrong-headed and will end in tears, so it's time to get bearish." Such approaches can be fatal to portfolio returns.

Mauldin the Republican

My antennae started to tingle when I read the writings of well-known newsletter writer and author John Maudlin, who has revealed his Texas Republican ties in the past. What I found disturbing was the way Mauldin wore his political views on his investment sleeve in this article entitled "Where's the Growth?" in which he attributed everything that`s wrong with the US economy to Keynesians and neo-Keynesians. Mauldin went on to attack Larry Summers for his secular stagnation thesis this way:

Launched by Larry Summers last November, a meme is burning its way through established academic economic circles: that we have entered into a period of – gasp! – secular stagnation. But while we can see evidence of stagnation all around the developed world, the causes are not so simple that we can blame them entirely on the free market, which is what Larry Summers and Paul Krugman would like to do: “It’s not economic monetary policy that is to blame, it’s everything else. Our theories worked perfectly.” This finger-pointing by Keynesian monetary theorists is their tried and true strategy for deflecting criticism from their own economic policies.

Neo-Keynesians have, in effect, messed up everything and their theories are to blame:

Where orthodox neo-Keynesian policies like large-scale deficit spending and aggressive monetary easing have been resisted – as in Japan years ago or in the Eurozone debtor countries today – lingering depressions are commonly interpreted as tragic signs that “textbook” neo-Keynesian economic policy could have prevented the pain all along and that weak economic conditions persist because governments and central banks are not doing enough to kick-start aggregate demand and stimulate credit growth at the zero lower bound.In essence, Mauldin is saying "my theory is better than your theory" (emphasis added):

In places like the United States and Japan, where neo-Keynesian thought leaders have already traded higher public debt levels and larger central bank balance sheets for unspectacular economic growth and the kinds of asset bubbles that always lead to greater instability in the future, their policies have failed to jump-start self-accelerating recoveries. Even in the United States, when QE3 has been fully tapered off, I would expect to see the broader economy start to lose momentum once again.

We’ve tried countercyclical deficit spending to resist recessions, procyclical (and rather wasteful) deficit spending to support supposed recoveries, and accommodative monetary easing all along the way (to lower real interest rates and ease the financing of those pesky deficits); but growth has been sluggish at best, inflation has been hard to generate, and labor market slack is making it difficult to sustain inflation even when real interest rates are already negative.

Call me a heretic, but I take a different view than the economists in charge. To my mind, the sluggish recovery is a sign that central banks, governments, and, quite frankly, the “textbook” economists (despite their best intentions) are part of the problem. As Detlev Schlichter commented in his latest blog post (“Keynes was a failure in Japan – No need to embrace him in Europe”), “To the true Keynesian, no interest rate is ever low enough, no ‘quantitative easing’ program ever ambitious enough, and no fiscal deficit ever large enough.” It’s apparently true even as debt limits draw closer.

While the academic elites like to think of economics as a reliable science (with the implication that they can somehow control a multi-trillion-dollar economy), I have repeatedly stressed the stronger parallel of economics to religion, in the sense that it is all too easy to get caught up in the dogma of one tradition or another. And all too often, a convenient dogma becomes a justification for those in power who want to expand their control, influence, and spending.In the following week`s article, Mauldin went on to criticize an over-reliance on monetary policy:

Whereas an Austrian or monetarist approach would suggest less government and a very light handle on the monetary policy tiller, Keynesian philosophy gives those who want greater government control of the economy ample reasons to just keep doing more.

Monetary policy has been able to mask a multitude of our government’s fiscal sins. My worry for the economy is what will happen when Band-Aid monetary policy can no longer forestall the hemorrhaging of the US economy. Long before we get to 2024 we will have a crisis. In past years, I have expected the problems to come to a head sooner rather than later, but I have come to realize that the US economy can absorb a great deal of punishment. But it cannot absorb the outcomes depicted in those last two charts. Something will have to give.Lower deficits and sound fiscal policy is the way to go, in his opinion. This will not end well (emphasis added):

And these projections assume there will be no recession within the next 10 years. How likely is that? What happens when the US has to deal with its imbalances at the same time Europe and Japan must deal with theirs? These problems are not resolvable by monetary policy.

An even scarier scenario is what will happen if we don’t deal with our fiscal issues. You can’t solve a yawning deficit with monetary policy.Notwithstanding the fact that the great austerity experiments in Europe have been unmitigated disasters, it seems futile to argue with someone for whom a theory represents a form of religious doctrine. From reading John Mauldin, I seriously question how much his views color the hedge fund managers and portfolios that he offers.

Further, at some point the velocity of money is going to reverse, and monetary policy will have to be far more restrained. The only reason, and I mean only, that we’ve been able to get away with such a massively easy monetary policy is that the velocity of money has been dropping consistently for the last 10 years. The velocity of money is at its lowest level since the end of World War II, but it is altogether possible that it will slow further to Great Depression levels.

When the velocity of money begins to once again rise – and in the fullness of time it always does – we are going to face the nemesis of inflation. Monetary policy during periods of inflation is far more constrained. Quantitative easing will not be the order of the day.

For Keynesians, we are in the Golden Age of Monetary Policy. It can’t get any better than this: free money and low rates and no consequences (at least no consequences that can be seen by the public). This will end, as it always does…

The Ritholz climate change obsession

I am not just trying to pick on John Mauldin and his conservative views. On the other side of the political aisle, Barry Ritholz seems to have an obsession with climate change, as evidenced by this recent tweet:

Here is just a small sample of the posts from his The Big Picture blog on this topic:

- Inaction on climate change

- Flooding risk from climate change, country by country

- Climate change: The scientific debate

- Significant climate change anomalies June 2014

To his credit, I have not seen Barry's climate change concerns creep into his investment views. I have not seen him has write anything to the effect that current policies are likely to lead to disaster, so therefore portfolios should be positioned for that outcome. Nor have I seen him advocate for financing such *ahem* speculative projects like this in Boston.

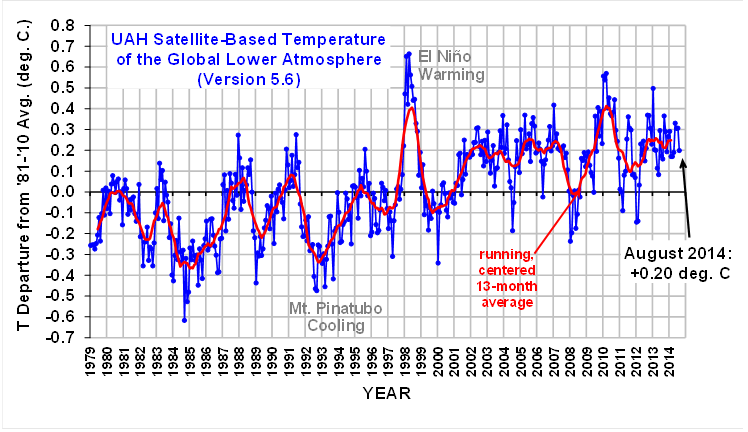

As investors, I believe that we should always be aware and be flexible about the limitations of our models. When the data doesn't fit the model, what do you do? While I understand that ecological time frames are different from investment time frames, but consider this chart of the pause in warming trends over the past decade:

Imagine a manager who has an investment theme that isn't working out. What is the procedure for decide on whether to stick to his guns and what is the procedure for re-examining and re-validating his models? The answer can be revealing of the thought processes that drive that manager's investment philosophy and process.

As investors, I believe that we should always be aware and be flexible about the limitations of our models. When the data doesn't fit the model, what do you do? While I understand that ecological time frames are different from investment time frames, but consider this chart of the pause in warming trends over the past decade:

{kind=link}

Imagine a manager who has an investment theme that isn't working out. What is the procedure for decide on whether to stick to his guns and what is the procedure for re-examining and re-validating his models? The answer can be revealing of the thought processes that drive that manager's investment philosophy and process.

The right way to be a Fed hater

To sum up, I reiterate my position that it`s perfectly normal to hold political views. Just don`t let them affect your portfolios.

I demonstrate this by singling out a very unique group - the Fed haters. Fed haters are a special species of investors who generally believe that what the Fed is doing is ultimately inflationary and, ultimately, the Fed will lose control of its policy and the US will get caught up in an inflationary spiral.

Again, it's ok to hold that view. Stan Druckenmiller is an example of an investor who is able to hold such views and effectively manage his portfolio. In 2013, Druckenmiller admitted that his models don't work anymore and he is a wash-up manager because Fed policies have distorted everything (via Business Insider):

In an interview with Goldman Sachs earlier this year, Druckenmiller sounded equally futile about his place in an easy-money, QE market. He, like a lot of hedge fund managers, has been critical of Fed Chair Ben Bernanke's policies.Bill Fleckenstein is another well-known investment professional who is a Fed-hater, but he also knows the limitations of his approach (via Business Insider).

Unlike other hedge fund managers, though, he's open about his own feelings of inadequacy because of those policies.

It has become harder for me, because the importance of my skills is receding. Part of my advantage, is that my strength is economic forecasting, but that only works in free markets, when markets are smarter than people....

It's not predicting anything the way it used to and that really makes me reconsider my ability to generate superior returns. If the most important price in the most important economy in the world is being rigged, and everything else is priced off it, what am I supposed to read into other price movements?

In a new interview with King World News, long-time Fed-critic Fleckenstein addresses the startling shouting match he got into with CNBC anchor Jackie DeAngelis on Tuesday.Despite his reservations about Fed policy, Fleckenstein closed his short selling fund in 2009 and he is in the process of re-starting it now:

For years, Fleckenstein had been warning investors through interviews that the loose monetary policies of the various developed market central banks would end in financial catastrophe.

And the manner in which he sounded his warnings made it seem as if this doom would be somewhat imminent.

"At what point are you willing to concede that you've misunderstood monetary policy?" DeAngelis asked point blank.

This had Fleckenstein understandably incensed.

"I don't misunderstand monetary policy," he responded. "I closed my short fund in 2009 because I knew the Fed would print money ... If you want to pursue idiots like the Fed, and their crazy policies, and you think you can get out in time, go for it."

Investing vs. policy

Ironically, one of the most interesting insights comes from the New York Fed at its blog, Liberty Street Economics. In this post, the author examined the differences in opinion in the future of interest rates between FOMC members (SEP) and the Survey of Primary Dealers (SPD):

The chart below shows the disagreement, as measured by the interquartile range, among participants in the SPD and the SEP for two-year-ahead projections of the FFR. While there is some dispersion among primary dealers’ forecasts, FOMC members have disagreed considerably more over the past three years.

Why are FOMC members more varied in their opinion of future interest rates than dealers? The answer is simple. Fed policy makers are more focused on how the economy is likely to change in light of their theories, which can vary widely. The dealers are just more pragmatic about the policy outlook (emphasis added):

Overall, the FOMC has tended to disagree more about the path of the FFR than market participants. One potential explanation for the difference is that FOMC members have disagreed more about the outlook for unemployment and inflation. However, we can’t rule out that private-sector participants disagree less about the outlook because they disagree less about the future path of the policy rate. That said, disagreement about unemployment in the longer-run should not be driven by policy expectations, and disagreement about this variable, at least until very recently, has been lower in the SPD than in the SEP. In addition, even if disagreement about the outlook in both surveys is the same, we should expect the FOMC to disagree more because private forecasters attempt to predict the most likely policy outcomes, whereas FOMC members report their views on the appropriate path for the FFR. That is, the dots represent policy prescriptions of each FOMC participant, rather than forecasts.

The 9 rules of investing

Academics focus on being right. Investment professionals focus on making money. Don`t confuse the two.

Ned Davis' nine rules of research are highly applicable in this instance:

Ned has 9 Rules of Research that all strategy team members follow and learn quickly when working at Ned Davis Research:

- Don’t Fight the Tape – the trend is your friend, go with Mo (Momentum that is)

- Don’t Fight the Fed – Fed policy influences interest rates and liquidity – money moves markets.

- Beware of the Crowd at Extremes – psychology and liquidity are linked, relative relationships revert, valuation = long-term extremes in psychology, general crowd psychology impacts the markets

- Rely on Objective Indicators – indicators are not perfect but objectively give you consistency, use observable evidence not theoretical

- Be Disciplined – anchor exposure to facts not gut reaction

- Practice Risk Management – being right is very difficult…thus, making money needs risk management

- Remain Flexible – adapt to changes in data, the environment, and the markets

- Money Management Rules – be humble and flexible – be able to turn emotions upside down, let profits run and cut losses short, think in terms of risk including opportunity risk of missing a bull market, buy the rumor and sell the news

- Those Who Do Not Study History Are Condemned to Repeat Its Mistakes

You can hold any political view you want. Just be pragmatic when it comes to managing your portfolio.

3 comments:

I stopped reading Maudlin several years back when he tried to spin a yearly rise in copper - he had predicted the reverse - as a success. Since then I think he's missed all the bull market since the 2009 lows.

Political ranting is just as prevalent or even more so on the other side. Whenever you see the phrase "tax cuts for the rich" (upper income and cap gain tax rates are higher versus lower income than they were under Clinton) the writer is ranting.

Once again, I'm gratified to see I am reading the same bloggers you are. Mauldin does lucidly weave in some good views from other people though (see Grant Maynard Williams piece reproduced at Zero Hedge....."Things That Make You Go Hmmm... Like The Perfect 'Kondratieff Winter' Storm Ahead" ) to help make his point.

There are some nice seasonal metaphors, and historical war parallels there that describe how economically we have reached this point.

Donald Coxe is another one who allows a "mission creep" of sorts to affect his view on why things are the way he perceives them to be.

Perhaps its because Republicans are wired for fear based on studies showing they have a larger amygdala and smaller anterior cingulate (the part of the brain responsible for courage and optimism) in their brain. :)

As a reader one has to just cut through the chaff and pull out the wheat. A parallel from Hollywood, can be drawn from someone who used to enjoy Mel Gibson, Woody Allen and Clint Eastwood when they came into their purview. Their tainted real lives may have jaded there view of their excellent body of work. We must differentiate between their public and private faces.

Hi Cam,

thanks for this great article.

IMO your best article yet.

Post a Comment