Investing is really about imagining your future self — when you are older, working less or not at all, earning much less money. Paying for our retirement or your kids (or latter generations) educations.Let me try and put it a different way. In these pages, I spend a lot of time focusing on returns that I sometimes forget my assumptions that my readers may not understand some of the basics of financial planning. Then I came across the results of a Nationwide Funds survey that found that among individuals with $100,000 or more in investible assets, a quarter don't have a financial plan; and 40% of those without a plan doubt they will ever have one.

The ability to think far into the future — years and decades — is not something that comes easy. But it is essential in order to be a successful investor.

A quarter of potential investors have no financial plan and close to 40% of that group doesn't anticipate building one. One common reason: apathy.

“Our advice for individuals is to seek help and to really think about … not only their investment, but their financial future,” said Mike Spangler, president of Nationwide Funds, which surveyed 783 potential investors with a minimum of $100,000 in investible assets.

“The numbers were jarring for us,” he said.

How do you know when you'll get there?

Part of the problem is investors don't realize they need a roadmap, or think that retirement is too far off that they haven't thought about a roadmap [emphasis added]:

Mr. Spangler said part of the disparity in financial planning stems from the Generation Y and Generation X groups. Many of them haven't consulted a professional, possibly because they feel retirement is a far- off prospect, or because they gather most of their financial advice through other means, he said...I am reminded of this passage from Alice in Wonderland when I read the above quote:

“It's hard to reach a destination that you haven't charted a map to,” he said. “Find an adviser that is really looking into your concerns and meeting you on your terms.”

"Would you tell me, please, which way I ought to go from here?"

"That depends a good deal on where you want to get to," said the Cat.

"I don’t much care where--" said Alice.

"Then it doesn’t matter which way you go," said the Cat.

"--so long as I get SOMEWHERE," Alice added as an explanation.

"Oh, you’re sure to do that," said the Cat, "if you only walk long enough."

It's just a savings plan!

OK, maybe the term "financial plan" may sound overly intimidating. In too many instances, financial professionals like us throw out jargon like "financial plan" or "asset-liability management" to a public that have no idea of what we are talking about. So I'll make it simple: It's not an investment plan, it's a savings plan!

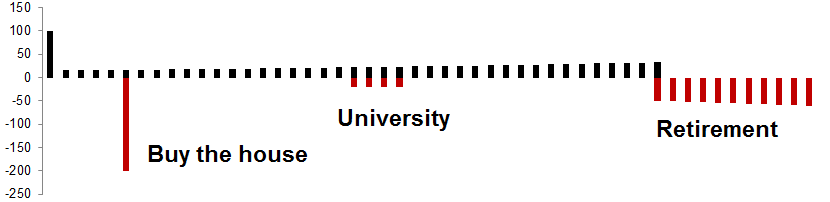

Here is a stylized diagram of a typical couple's cash flows might look like over the course of their lives. The grey bars above represent their savings and the red bars represent their future liabilities, or spending, over the course of their lives.

Stylized Cash Flow Projections

In this example, I assume that the couple just got married and have a modest nest egg. They plan to buy a house in the next few years, bring up a child and send him to university at the appropriate time in the future, and finally retire.

The

It's really that simple. Get a reasonable return on your savings, don't take too much risk and blow your financial brains out.

The part that confuses most people is the variability of returns. The prices of stocks, bonds and other investments change on a daily basis. In the short run, we spend far too much time chasing after extra returns and we forget about the longer term view of what it's all about - it's a savings plan.

In the short-run, capital market returns are hard to forecast. In the long run, forecasting returns are fairly easy. In a future post, I will write about how to forecast long-run stock market returns.

Cam Hui is a portfolio manager at Qwest Investment Fund Management Ltd. (“Qwest”). The opinions and any recommendations expressed in the blog are those of the author and do not reflect the opinions and recommendations of Qwest. Qwest reviews Mr. Hui’s blog to ensure it is connected with Mr. Hui’s obligation to deal fairly, honestly and in good faith with the blog’s readers.”

None of the information or opinions expressed in this blog constitutes a solicitation for the purchase or sale of any security or other instrument. Nothing in this blog constitutes investment advice and any recommendations that may be contained herein have not been based upon a consideration of the investment objectives, financial situation or particular needs of any specific recipient. Any purchase or sale activity in any securities or other instrument should be based upon your own analysis and conclusions. Past performance is not indicative of future results. Either Qwest or I may hold or control long or short positions in the securities or instruments mentioned.

6 comments:

Financial planner is most important to a business . A financial planner are able to make a proper road map and can achieve

Annuity Columbia MD

Nice Blog. Thank you for sharing and I want to share information about the Cash Flow Navigator. Cash Flow Navigator is a Financial Planning Advisor. It provides free information and resources for their members to plan and achieve Financial Independence.

The key to achieving your goals tomorrow is creating a plan that starts today. A financial planner or advisor can help you understand all the options and create a financial plan just for you that will take all your long-term goals and short-term needs into consideration.

i will surely hire a Personal Financial Advisor for acheive my future goal.

Brilliant mind.. thank you for posting this article. I agree that when it comes to serious matters like finance, an expert is definitely needed. Financial experts should provide clients with advice on financial matters, always have recommendations on ways to best spend their money. Make sure to involve himself in researching the marketplace and advising clients on products and services available, ensuring they are aware of and understand those that best meet their needs.

Brilliant mind.. thank you for posting this article. I agree that when it comes to serious matters like finance, an expert is definitely needed. Financial experts should provide clients with advice on financial matters, always have recommendations on ways to best spend their money. Make sure to involve himself in researching the marketplace and advising clients on products and services available, ensuring they are aware of and understand those that best meet their needs.

Sticking to the financial plan would be the most difficult step to follow. However, I am sure the above ideas about financial planning advice will help most of the people who doesn't follow a rigid flow-chart of their daily schedules.

When I was not having a proper financial plan, I use to empty the pocket and wallet in no time. A proper planning not only helps to monitor the daily expenses but also, it helps a lot to live the whole month without any money shortage.

Great tips successful financial planning! Thank you....

Post a Comment