As a reminder, the signals of the Trend Model are out-of-sample signals, but there are no portfolio returns to publish, mainly because I don't know anything about you. I know nothing about your return targets, your risk tolerance and pain thresholds, your tax situation, or even the jurisdiction you are in. If I offered an actual portfolio, it would be a formal prospectus document outlining what to expect.

Instead, the backtested returns are based on a specific formula for constructing a balanced fund portfolio based on Trend Model scores and reasonable risk assumptions of an average investor with a 60% stock/40% bond asset allocation.

- Risk-on: 80% SPY (S&P 500), 20% IEF (7-10 Treasuries)

- Neutral: 60% SPY, 40% IEF

- Risk-off: 40% SPY, 60% IEF

An advisor or portfolio manager could then change the equity allocation by 20% depending on the Trend Model score without Compliance tapping him on the shoulder.

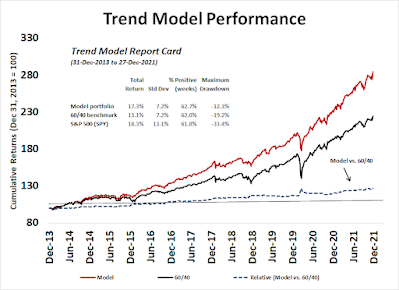

The historical backtest of the Trend Model using this portfolio construction technique yielded excellent results. An investor using this approach could achieve equity-like returns while bearing balanced fund-like risk. Needless to say, this backtest is just a proof of concept. Every investor is different and your mileage will vary.

A reader then asked me to backtest a more aggressive approach to portfolio construction. Instead of a 60% SPY and 40% IEF benchmark, he suggested a 100% equity position, based on 60% SPY and 40% defensive equity substitute for bonds. The defensive portfolio consists of an equal-weighted portfolio of XLV (Healthcare), XLP (Consumer Staples), XLU (Utilities), and XLRE (Real Estate).

The results turned out to be a case of "penny wise, pound foolish".

The full post can be found here.

No comments:

Post a Comment