Still, there are still nagging doubts about pockets of hidden financial leverage in the banking system. Is there another shoe waiting to drop?

The full post can be found here.

Turkish central bank Governor Sahap Kavcioglu said markets shouldn’t take for granted that he’ll cut interest rates as soon as April, when he sets monetary policy for the first time since his surprise appointment.

“I do not approve a prejudiced approach to MPC decisions in April or the following months, that a rate cut will be delivered immediately,” Kavcioglu said in a written response to questions emailed by Bloomberg News, referring to monetary policy committee meeting next month.

“In the new period, we will continue to make our decisions with a corporate monetary policy perspective to ensure a permanent fall in inflation. In this respect, we will also monitor the effects of the policy steps taken so far,” Kavcioglu said.

We maintain several market timing models, each with differing time horizons. The "Ultimate Market Timing Model" is a long-term market timing model based on the research outlined in our post, Building the ultimate market timing model. This model tends to generate only a handful of signals each decade.

Two of the world’s largest sovereign wealth funds say investors should expect much lower returns going forward in part because the typical balanced portfolio of 60/40 stocks and bonds no longer works as well in the current rate environment.Singapore’s GIC Pte and Australia’s Future Fund said global investors have relied on the bond market to simultaneously juice returns for decades, while adding a buffer to their portfolio against equity market risks. Those days are gone with yields largely rising.“Bonds have been in retrospect this gift,” with a 40-year rally that has boosted all portfolios, said Sue Brake, chief investment officer of Australia’s A$218.3 billion ($168.4 billion) fund. “But that’s over,” she added, saying “replacing it is impossible -- I don’t think there’s any one asset class that could replace it.”Thanks to declining returns from bonds, the model 60/40 portfolio may eke out real returns -- after inflation -- of just 1%-2% a year over the next decade, said Lim Chow Kiat, chief executive officer of GIC. That compares with gains of 6%-8% over the past 30 to 40 years, he said.

Norway’s $1.3 trillion sovereign wealth fund has already made the shift, winning approval to adjust its equity-bond mix to 70/30 in 2017. At the end of last year, it held about 73% in equities, and 25% in bonds.

Mid-week market update: The rebound in the NASDAQ and growth stocks was not a surprise. Value outperformed growth by the most on record last week - and that includes the dot-com crash that began in 2000.

Make no mistake. Growth stocks are experiencing an unsustainable dead cat bounce.

The full post can be found here.

Recently, I learned a fact about our company that I had never suspected: Berkshire owns American-based property, plant and equipment – the sort of assets that make up the “business infrastructure” of our country – with a GAAP valuation exceeding the amount owned by any other U.S. company. Berkshire’s depreciated cost of these domestic “fixed assets” is $154 billion. Next in line on this list is AT&T, with property, plant and equipment of $127 billion.

Our leadership in fixed-asset ownership, I should add, does not, in itself, signal an investment triumph. The best results occur at companies that require minimal assets to conduct high-margin businesses – and offer goods or services that will expand their sales volume with only minor needs for additional capital. We, in fact, own a few of these exceptional businesses, but they are relatively small and, at best, grow slowly.

The full post can be found here.

Preface: Explaining our market timing models

We maintain several market timing models, each with differing time horizons. The "Ultimate Market Timing Model" is a long-term market timing model based on the research outlined in our post, Building the ultimate market timing model. This model tends to generate only a handful of signals each decade.

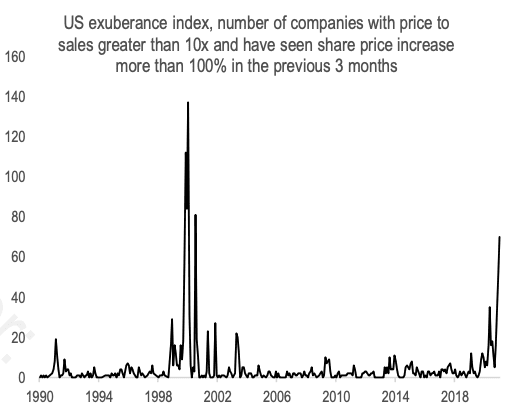

There is a very big divergence in the readings across stocks. Some stocks are, by these measures, in extreme bubbles (particularly emerging technology companies), while some stocks are not in bubbles.