Five years after the U.S. economy faced its most serious crisis since the Great Depression, a majority of Americans (63%) say the nation’s economic system is no more secure today than it was before the 2008 market crash. Just a third (33%) think the system is more secure now than it was then.

Large percentages say household incomes and jobs still have yet to recover from the economic recession. And when asked about the impact of government efforts to deal with the recession, far more believe that economic policies have benefitted large banks, corporations and the rich than the middle-class, the poor or small businesses.

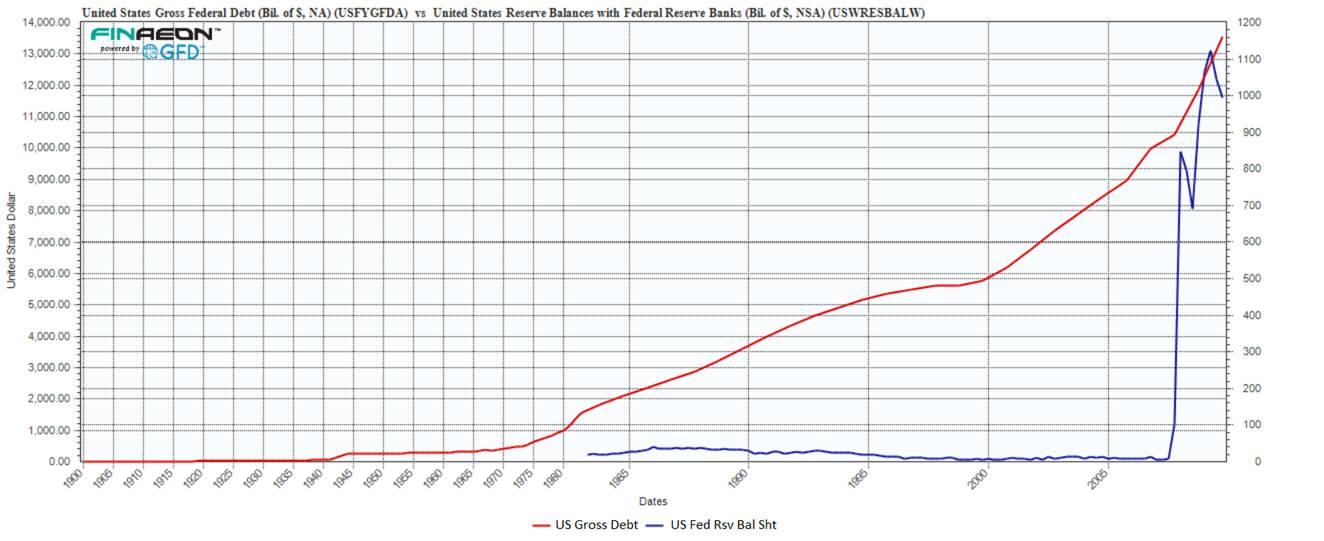

What happened to "unchecked greenback emissions"?

What have we learned? I learned that, in the aftermath of the collapse, a lot of experts were wrong, or more charitably characterized as "early", in their forecasts of the effects of the collapse and the policy response to the collapse. Consider the prognostication of no less a luminary than Warren Buffett, who warned about the effects of money printing and deficit spending in a NY Times Op-Ed on August 18, 2009:

Our immediate problem is to get our country back on its feet and flourishing — “whatever it takes” still makes sense. Once recovery is gained, however, Congress must end the rise in the debt-to-G.D.P. ratio and keep our growth in obligations in line with our growth in resources.

Unchecked carbon emissions will likely cause icebergs to melt. Unchecked greenback emissions will certainly cause the purchasing power of currency to melt. The dollar’s destiny lies with Congress.

The policy and market response

What has happened since then? The federal deficit has soared and so has the Fed's balance sheet. The chart below from Global Financial Data shows the policy response:

What about the market response? The USD didn't plummet in the wake of "unchecked greenback emissions", largely because of the global nature of the financial crisis. Other major industrialized countries (and the eurozone in particular) experienced their own financial crisis and global central bankers went into crisis mode. The balance sheets of the ECB, BoE, BoJ and other central banks expanded to stratospheric levels in response. In that case, shouldn't the effects show up in inflation rather than then the exchange rate? Inflation, as measured by the CPI, has been extremely tame. What about commodity inflation? Shouldn't it show up as commodity inflation? Well, sort of. As the chart below shows, commodity prices (in black) did rise in the wake of the global financial crisis, but so did stock prices (in red). Commodity prices peaked out in early 2011, but stock prices have continued to advance.

Where's the inflation?

Inflation has been dormant

Perhaps the forecasters are early. Some analysts, such as David Rosenberg, believe that stagflation lies in our future:

You cannot keep real short-term rates negative for this long in the face of even modestly positive real economic growth without generating financial excesses today and inflationary pressures in the future. That’s why I continue to believe that the next major theme — and the legacy of the Ben Bernanke regime — will be stagflation.Warren Buffett expressed his concerns about stagflation back in 2008, according to Bloomberg:

``We're right in the middle of it right now,'' said Buffett, chairman of Omaha, Nebraska-based Berkshire Hathaway Inc., in an interview on Bloomberg Television today. ``I think the `flation' part will heat up and I think the `stag' part will get worse.''Though he was uncertain about its timing:

``It's not going to be tomorrow, it's not going to be next month, and may not even be next year,'' said Buffett, 77.Stagflation involves two elements, slow growth and inflation. I understand the slow growth part of the stagflation forecast. The growth path of the American economy remains anemic, largely because this is not the typical recovery from an inventory recession, but a balance sheet recession that requires the deleveraging of household, corporate and government balance sheets. That process takes time.

I am not sure I get the inflation part of the forecast. Today, five years after the Lehman Crisis, we have see little signs of consumer price inflation and asset inflation, in the form of commodity price inflation, remains relatively tame. How long do we have to wait?

Is inflation purely a monetary phenomena?

It sounds like that that the model underlying the thinking of people like Rosenberg and Buffett is Milton Friedman's MV=PQ conceptual framework:

is the total amount of money in circulation on average in an economy during the period, say a year.

is the total amount of money in circulation on average in an economy during the period, say a year. is the transactions velocity of money, that is the average frequency across all transactions with which a unit of money is spent. This reflects availability of financial institutions, economic variables, and choices made as to how fast people turn over their money.

is the transactions velocity of money, that is the average frequency across all transactions with which a unit of money is spent. This reflects availability of financial institutions, economic variables, and choices made as to how fast people turn over their money. and

and  are the price and quantity of the i-th transaction.

are the price and quantity of the i-th transaction. is a column vector of the , and the superscript T is the transpose operator.

is a column vector of the , and the superscript T is the transpose operator. is a column vector of the .

is a column vector of the .If you were to increase the money supply by expanding the Fed balance sheet, holding V (velocity) and Q (quantity produced in the economy) constant, price rises and you get inflation. That's why, it is said, that inflation is a monetary phenomena.

So far, despite the Fed's efforts to expand the monetary base, velocity has collapsed and we have seen little signs of inflation.

A demographic explanation

To resolve this conundrum, it might be useful to study the last episode of stagflation. Steve Randy Waldman recently proposed an alternative explanation of the stagflation of the 1970's based on age demographics, namely that stagflation was the result of stagnant productivity, not just money printing. Consider the chart below of US productivity. It was stagnant during the 1970's but it has soared to new highs in the current post-Lehman Crisis period.

Waldman wrote:

The “malaise” of the 1970s was not a problem with GDP growth. NGDP growth was off the charts (more on that below). But real GDP growth was strong as well, clocking in at 38%, compared to only 35% in the 1980s, 39% in the 1990s, and an abysmal 16% in the 2000s.Simply put, there were too many Baby Boomers entering the workforce at that time and productivity lagged as a result:

What was stagnant in the 1970s was productivity, which puts hours worked beneath GDP in the denominator. Boomers’ headlong rush into the labor force created a strong arithmetic headwind for productivity stats.

The root cause of the high-misery-index 1970s was demographics, plain and simple. The deep capital stock of the economy — including fixed capital, organizational capital, and what Arnold Kling describes as “patterns of sustainable specialization and trade” — was simply unprepared for the firehose of new workers. The nation faced a simple choice: employ them, and accept a lower rate of production per worker, or insist on continued productivity growth and tolerate high unemployment. Wisely, I think, we prioritized employment. But there was a bottleneck on the supply-side of the economy. Employed people expect to enjoy increased consumption for their labors, and so put pressure on demand in real terms. The result was high inflation, and would have been under any scenario that absorbed the men, and the women, of the baby boom in so short a period of time. Ultimately, the 1970s were a success story, albeit an uncomfortable success story. Going Volcker in 1973 would not have worked, except with intolerable rates of unemployment and undesirable discouragement of labor force entry. By the early 1980s, the goat was mostly through the snake, so a quick reset of expectations was effective.Policy makers, in effect, wanted to avoid more social tensions and unrest (remember the anti-Vietnam sentiment of the early 1970's) and paid the price in the form of slow growth and rising inflation. Karl Smith, writing in Forbes, quoted Arthur Burns in justifying the high inflation of the 1970's:

“Viewed in the abstract the Federal Reserve System had the power to abort the inflation in its incipient stage fifteen years ago or at any later point, and it has the power to end it today. At any time during that period, it could have restricted the money supply and created sufficient strains in financial and industrial markets to terminate inflation with little delay. It did no do so because the Federal Reserve was itself caught up in the philosophic and political currents that were transforming American life and culture.Smith went on:

Put another way, high inflation can always be prevented if one is willing to tolerate recessions. Yet, recessions have consequences. Government budgets – at minimum – are redirected towards immediate relief, if not outright cut. Public investments in basic research, exploration and state-of-the-art infrastructure are postponed. In the private sector R&D budgets are slashed and new products put on hold. Small businesses, especially young start-ups, perish en masse. Families who are just beginning to climb the socioeconomic ladder and offer a better future to their children are knocked back down. Social tensions rise. Xenophobic and ethnocentric movements flourish. The adolescent generation, just on its way to the workforce, is permanently marred by a shortage of training and experience.If demographics was the main cause of the stagflation of the 1970's, then stagflation may not be in our immediate future. In fact, a paper by IMF economist Patrick Imam (via Business Insider) suggests that an aging population is likely to make monetary policy less effective. Michael Mandel wrote a paper suggesting that productivity growth is likely to skyrocket in the near future because of technological innovations. As well, Izabella Kamanska chimed in and wrote on the likely deflationary effects of a global population peak.

Investment implications

Who is right? David Rosenberg and Warren Buffett in forecasting stagflation, or at least, rising inflation in our future? Or the likes of Waldman, who proposed a demographic and productivity explanation of the stagflation of the 1970's, whose implication is that rising productivity will act to contain inflation?

For policy makers, it presents a conundrum. Who do you believe? Policy makers have a much more difficult problem because policy is dependent on the underlying model of how the economy works.

For investors, the conundrum can be resolved easily because they don't have to adhere to any single point of view. The answer is model diversification.

I honestly don't know who is right. However, my inner investor believes that he should stay flexible and create a portfolio that diversifies between models.

For me, my investment lesson learned in the aftermath of the Lehman Crisis is not to be overly dogmatic about your economic and political beliefs. Stay flexible and learn to diversify your models.

Cam Hui is a portfolio manager at Qwest Investment Fund Management Ltd. (“Qwest”). The opinions and any recommendations expressed in the blog are those of the author and do not reflect the opinions and recommendations of Qwest. Qwest reviews Mr. Hui’s blog to ensure it is connected with Mr. Hui’s obligation to deal fairly, honestly and in good faith with the blog’s readers.”

None of the information or opinions expressed in this blog constitutes a solicitation for the purchase or sale of any security or other instrument. Nothing in this blog constitutes investment advice and any recommendations that may be contained herein have not been based upon a consideration of the investment objectives, financial situation or particular needs of any specific recipient. Any purchase or sale activity in any securities or other instrument should be based upon your own analysis and conclusions. Past performance is not indicative of future results. Either Qwest or I may hold or control long or short positions in the securities or instruments mentioned.

4 comments:

Hi Cam,

Thanks for constantly educating us by bringing out varied points-of-views. I really enjoy being able to get a synopsis of different POVs by other economists and investment professional. So your post leads to further questions:

I: So what sectors/industries do well during stagflation? I would imagine Real estate would be one.

II: What other than tech does well during productivity gains, i.e. opposite of stagflation or -what would be considered- "normal times"?

Thanks again.

One of your best posts yet Cam, and that's saying something. As always, thank you for sharing your detailed thoughts.

Thank you for the post. The question remains: Diversify into what and keep the net result positive how? What happens to bonds and stocks if/when interest rates go up? And what happens if interest rates are kept low for a very long time (Japan)? And which currencies seem strong to you? And how will real estate markets do as an indebted aging population liquidates? One could go on, but more specific scenarios would help the humble readers better understand what you would do for your clients and why come back to read this blog.

This is a very informative article. I was looking for these things and here I found it. I am doing a project and this information is very useful to me. I always try to find information and hopefully I found more about what I am looking for.

Post a Comment